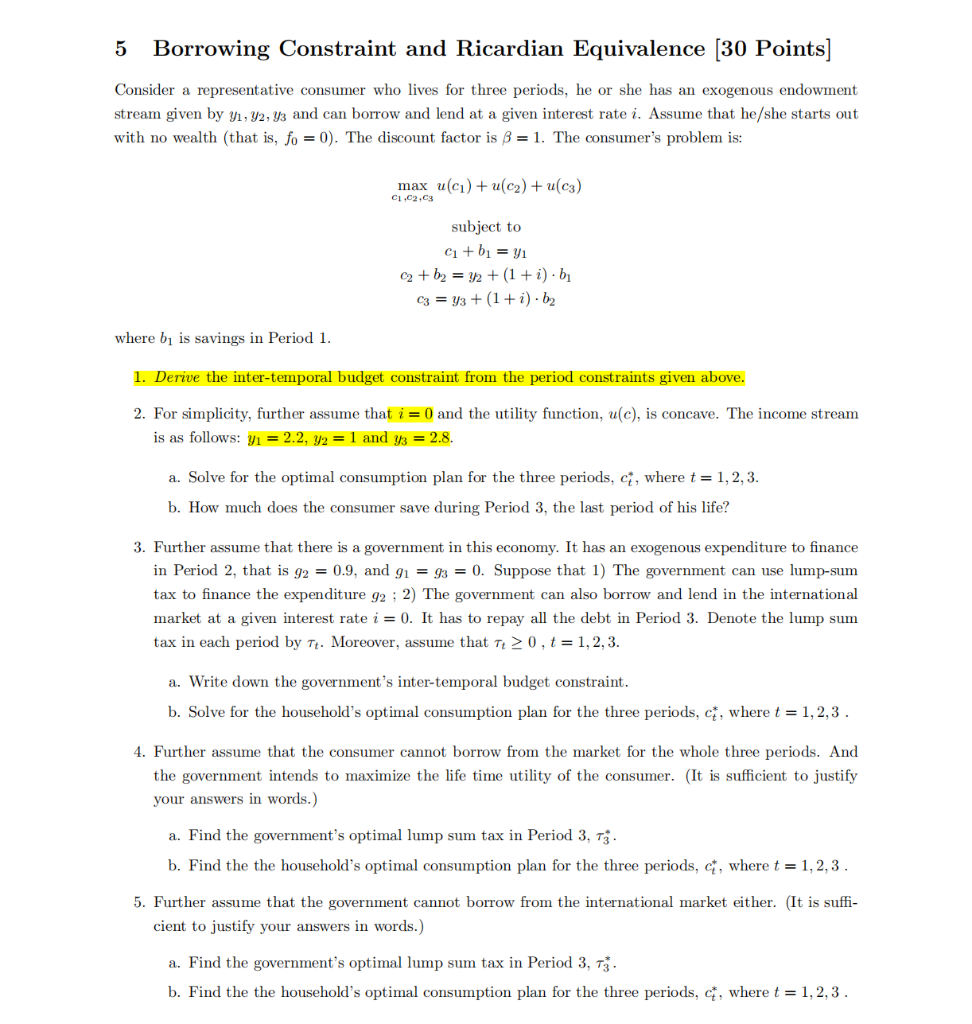

Precisely why individuals favor small-term mortgages would be to save money. Due to the fact large monthly obligations is dissuade some borrowers, these types of loans come with smaller notice, possibly preserving thousands of cash along the longevity of the loan. The faster you only pay regarding the loan harmony, the faster you then become brand new outright proprietor of the property.

Why should you need a short-name financial?

As well, an initial-title mortgage allows you to be financial obligation-100 % free reduced, releasing right up cashflow to other possibilities such financial investments otherwise investing of other sorts of obligations. This will work for borrowers of various age groups, helping all of them end up being residents faster whenever you are removing monthly home loan repayments in this simply ten years or reduced.

Yes, you can re-finance your existing home loan to an initial-title financial to reduce your interest rate and you can rescue currency along side life of the mortgage. Definitely, you ought to just do this if you’re able to afford the large monthly premiums. Refinancing helps you pay your own mortgage reduced whether or not it is sensible for your requirements for how much you’ve already paid on the financial.

Nevertheless, you can easily pay off their mortgage loan in less time, letting you easily build guarantee or take a quicker channel so you’re able to homeownership.

Think about, an element of the reason for refinancing their mortgage is to obtain ideal terms and conditions and take advantage of the current security of your home. Shortening the duration of your mortgage means big payments but saving much more during the interest over time. At the same time, stretching your home loan label mode lowering your monthly obligations https://paydayloanalabama.com/coats-bend/ while paying a whole lot more from inside the appeal over time. Which choice is good for you relies upon your unique finances.

Such as, you might refinance so you’re able to a preliminary-label home loan if you’ve has just received promoted otherwise earn more income today, allowing you to pay off the financial faster because you find the money for do so.

How to find out whether I will afford a preliminary-title mortgage?

Finding out whether you can afford a primary-term home mortgage is similar means you’d ascertain if you really can afford whichever home loan. You will have to check out the loan amount, interest, mortgage terms, mortgage insurance coverage, HOA fees, and taxation to determine how much cash home you can afford.

As a general rule away from thumb, only about twenty-eight% of your gross income should go so you can paying your financial. Therefore, for people who secure $100,000 annually, you should only spend $twenty-eight,000, otherwise $dos,333 per month, toward home financing. As well, the mortgage need to make right up just about thirty six% of complete personal debt.

While Va eligible, you can use the Virtual assistant finance calculator to compare a 30-12 months Virtual assistant financing and you may a good fifteen-seasons Virtual assistant mortgage to choose hence choice is better for you.

Needless to say, the entire cost of your loan may also be influenced by your advance payment, DTI, credit history, and newest rates of interest. The only way to learn if you really can afford a short-label mortgage loan would be to correspond with a lender.

The home loan specialist helps you see whether you can afford a preliminary-label mortgage and exactly how far home you can afford by the researching your revenue and you can costs when you are factoring various other financial factors including credit history.

Statement Lyons is the Maker, Chief executive officer & Chairman from Griffin Resource. Mainly based inside 2013, Griffin Financial support was a nationwide shop lending company emphasizing providing 5-star provider so you’re able to their subscribers. Mr. Lyons has actually twenty-two many years of experience in the mortgage organization. Lyons can be regarded as a market frontrunner and you can professional within the genuine property fund. Lyons has been featured from inside the Forbes, Inc., Wall surface Path Log, HousingWire, and more. Since a member of the mortgage Bankers Relationship, Lyons could possibly keep up with important alterations in the fresh new industry to send the quintessential really worth in order to Griffin’s customers. Around Lyons’ management, Griffin Financial support made the latest Inc. 5000 quickest-broadening people checklist 5 times within its ten years running a business.

Likewise, long-name mortgages, instance a 30-seasons mortgage, are typical because they provide borrowers more hours to repay the money. Which have stretched installment periods, borrowers spend shorter monthly however, a whole lot more during the attract across the lives of your own loan.

- Faster approach to homeownership: Which have quick-term mortgages, you possess your home quicker than simply having 30-year mortgage loans. It indicates once just ten years (or less), you are able to individual your residence and avoid and come up with home loan repayments, allowing you to cut back with other investments.